Every time you walk into a doctor’s office, you’re not just handing over your health information-you’re also handing over your financial trust. And for too long, that trust has been exploited. In 2024, New York State changed the game with three new laws designed to stop healthcare providers from pushing patients into financial traps. These aren’t minor tweaks. They’re full-on protections built to shield you from surprise bills, forced credit applications, and shady consent forms that hide financial traps in plain sight.

Separate Consent for Treatment and Payment

For years, hospitals and clinics used one form to get your signature for both medical treatment and payment. You’d sign at check-in, thinking you were just agreeing to be seen. But that signature often locked you into paying with a medical financing plan-like CareCredit-without you even realizing it. That’s over. As of October 20, 2024, New York law requires providers to get two separate consents: one for your treatment, and one for any payment arrangement.

This means you can’t be pressured into signing a financial agreement while you’re anxious, in pain, or rushed through intake. If a provider tries to slip a payment form into your paperwork without your clear, separate approval, they’re breaking the law. Violations can cost them $2,000 per incident. That’s not a warning. That’s a fine. And it’s enforceable.

But here’s the catch: as of August 2025, enforcement of this specific rule (Public Health Law Section 18-c) has been suspended. That doesn’t mean it’s gone. It means the state is reviewing how it’s applied. Until then, providers are still expected to follow the spirit of the law. Don’t assume your consent is valid unless you’re given a standalone document about payment options-and given time to read it.

No More Filling Out Your Credit Applications for You

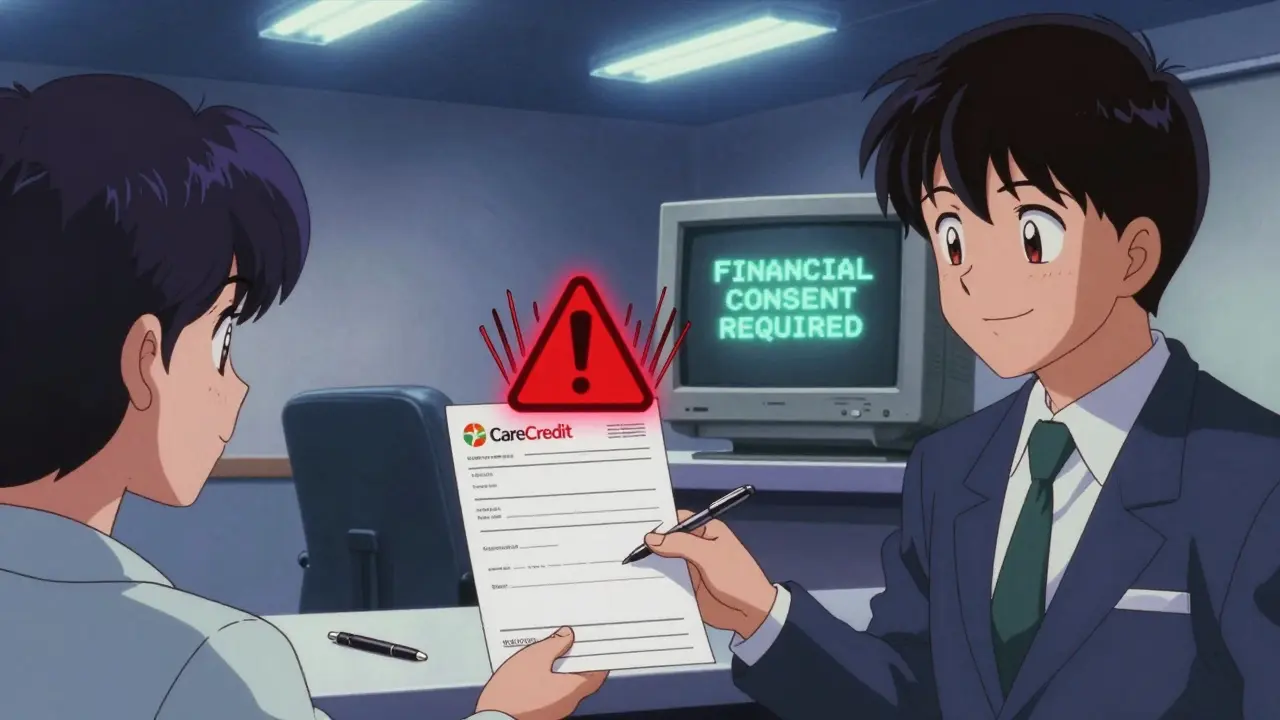

Have you ever been handed a CareCredit application at the front desk and told, “Just sign here”? That’s illegal now. General Business Law Section 349-g makes it a violation for any healthcare provider to complete even one field on your application for a medical financing product. That includes pre-filling your name, income, or employment details.

Providers can answer your questions. They can explain what CareCredit is. They can even hand you the form and point to where to sign. But if they touch the pen to the paper-even to help you fill out your address-they’re risking a $5,000 fine per violation. This law was created because too many patients ended up with debt they didn’t understand, often because staff pushed them into financing without explaining the interest rates or repayment terms.

It’s not about removing choice. It’s about removing pressure. You should be able to walk out with a treatment plan and a clear understanding of what you owe-and how you’ll pay-without anyone steering you toward a product that benefits the provider more than you.

Why Your Credit Card Is Riskier Than You Think

Most people think paying with a regular credit card is safe. It’s not. New York’s General Business Law Section 519-a specifically bans providers from requiring you to give them your credit card number before receiving emergency or medically necessary care. That means no more holding your card on file just because you “might need to pay later.”

But here’s the deeper issue: when you pay with a regular credit card, you lose legal protections. Medical debt that comes from healthcare-specific financing tools-like CareCredit, MediCard, or other medical credit lines-can’t be reported to credit bureaus under the CFPB’s 2024 rule. That’s right: medical bills on those products no longer hurt your credit score.

But if you use your Visa or Mastercard? That debt can still show up on your credit report. It can lead to wage garnishment. It can trigger liens on your home. It can be sold to collectors without your knowledge. New York law now requires providers to warn you about this every single time you use a traditional credit card for medical payments. That warning has to be clear, written, and given before you pay.

If you’ve ever been told, “We’ll just charge it,” and walked away without knowing the consequences-you now have the right to ask: “Is this going on my credit report?”

How This Compares to Federal Laws

The federal No Surprises Act, which took effect in January 2022, stops you from getting surprise bills from out-of-network providers. That’s huge. But it doesn’t touch what happens inside the office. New York’s laws go further. They protect you from financial manipulation even when you’re seeing an in-network doctor you’ve chosen yourself.

While federal law focuses on billing transparency, New York’s laws focus on consent, control, and fairness. They stop providers from turning your medical need into a sales opportunity. They prevent staff from pushing you into high-interest financing. They force clear communication about how your payment method affects your credit and your rights.

Other states are watching. Barclays Health Law Advisory predicted in late 2024 that New York’s model will be copied. And with over 100 million Americans carrying $195 billion in medical debt, it’s not a matter of if other states will follow-it’s when.

What You Should Do Now

You don’t need a lawyer to protect yourself. But you do need to know your rights. Here’s what to do before your next appointment:

- Ask: “Will I be asked to sign anything about payment?” If yes, ask to see it separately from your treatment consent.

- If someone offers you CareCredit or a similar product, ask: “What’s the interest rate? What happens if I can’t pay? Is this reported to credit bureaus?”

- Never let a provider fill out a financial application for you-even if they say it’s “just to help.”

- If you pay with a credit card, ask: “Will this payment be treated as medical debt or consumer debt?”

- Keep copies of all consent forms and payment disclosures. If something feels off, document it.

These laws aren’t perfect. The suspension of Section 18-c creates confusion. Not every provider has updated their systems. But they’re a step in the right direction. And if enough patients start asking questions, providers will have no choice but to comply.

Why This Matters Beyond New York

Medical debt isn’t just a New York problem. In 2022, 74.6 million Americans had medical debt. 50.8 million had it in collections. That’s not bad luck. That’s a system designed to profit from illness.

These laws shift the power back to the patient. They say: your health shouldn’t cost you your credit. Your pain shouldn’t be used to sell you debt. Your consent shouldn’t be hidden in fine print.

Even if you live in another state, this is a warning sign. If New York can do this, so can others. And if you’re being asked to sign something you don’t understand-especially around money-you now have the language to push back. You have the right to say no. You have the right to wait. You have the right to be treated like a person, not a revenue stream.

Knowledge is your best protection. Use it.